Abstract: Chen Yuandong, deputy secretary-general of the Coating Abrasives Branch, made a report on “Analysis of the Economic Operation of the Coated Abrasives Industry in 2015†in 2015. Facing the relatively complicated economic environment at home and abroad and increasing downward pressure, it is the same as many related industries. The coated abrasive industry has also encountered unprecedented...

Chen Yuandong, Deputy Secretary General of the Coated Abrasives Branch, made a report on "Analysis of Economic Operation of Coated Abrasives Industry in 2015"

In 2015, faced with the relatively complicated economic environment at home and abroad and the increasing downward pressure, like many related industries, the coated abrasive industry has encountered unprecedented difficulties. In particular, in the second half of the year, most enterprises were under-employed, product homogenization competition was fierce, prices fell, corporate accounts receivable increased, new projects were reduced, and enterprises suffered from cold winters. However, some enterprises have faced difficulties and actively responded to the challenges. They have taken the initiative to embark on the path of transformation and upgrading by relying on new products, new technologies and business innovations, and achieved good results. First, the overall operation of the industry throughout the year. (Club statistics)

1. Completion of major economic indicators of the industry :

output value

unit price

In the production of sand sheet, paper-based products were 232 million square meters (91.7%), and cloth-based products were 0.21 billion square meters (8.3%).

In the production of sand rolls, paper-based products were 23 million square meters (13.6%), and cloth-based products were 153 million square meters (86.4%).

The paper-based products in the products: 3,629,700 square meters. The paper base production value was 1.471 billion yuan (90.1%), and the cloth base was 162 million yuan (9.9%).

The output value of sand rolls is 237 million yuan (8.9%) and the cloth base is 2.429 billion yuan (91.1%).

Paper-based products in products: 0.83 billion yuan , the basic situation of operation.

In 2015, the total assets of the industry enterprises increased by 18.22%, the total liabilities increased by 30.27%, the total asset-liability ratio was 33.4%, an increase of 3.1 percentage points, at a reasonable level; the total profit was 525 million yuan, a slight increase of 0.56%, only one manufacturing enterprise. Loss. However, many companies are struggling near the break-even point, and the polarization of enterprises has further increased.

There are 26 of the 42 industrial enterprises with a median value of more than 50 million yuan, and 13 of them have more than 100 million yuan.

The total output value of 30 manufacturing enterprises was 4.849 billion yuan, a year-on-year decrease of 3.69%. The output value of 15 companies increased, and the unit price of 12 products rose. The top three values ​​of total output value and sand cloth production value are: Jiangsu Mitsubishi, Hubei Yuli, Jiangsu Fengmang. The top three production values ​​of sandpaper are: Zibo Sisha Taishan, Dongguan Golden Sun, and Changzhou Jinniu. The top three production value growth: Jiangsu Baolun Abrasives, Zhengzhou Jiayan, Baige Abrasives. The top three profit margins: Dongguan Golden Sun, Changzhou Jinniu, Jiangsu Mitsubishi.

The total output value of the 12 companies with statistics was 768 million yuan, a year-on-year increase of 1.32%. The output value of 5 enterprises increased, and the unit price of 6 companies rose. The top three output values ​​are: Sichuan Gurui, Anhui Brothers, and Linyi Sanchao. The top three output growth: Zhengzhou Baige, Meizhou Nanyu, Sichuan Gurui. The top three profit margins: Anhui brothers, Sichuan Gurui, Shunde Qi and rise.

Second, the import and export situation: (Customs data)

The import value of coated abrasives has been less than the export amount for three consecutive years. Although the export unit price has increased, the unit price of imported products is still 2.6 times of the export unit price. The trade surplus was $102 million, an increase of 37.9%.

1. The export volume is reduced by price.

The export volume of coated abrasives decreased by 2.95% year-on-year, the export value (slightly), and the export unit price (slightly) increased by 8.69%.

The export products are mainly sand cloth, accounting for 43.6% of the total export of coated abrasives, the amount (slightly), and the unit price is 3.88 US dollars / kg.

Export sandpaper accounts for 41% of the total export value, the amount (slightly), the unit price is 4.37 US dollars / kg.

Exporting other substrate coated abrasives accounted for 14.3% of the total export value, the amount (omitted), the unit price of 14.34 US dollars / kg.

From the export of coated abrasives in China:

The top three exporters of sand cloth are Vietnam, the United States, and South Korea, accounting for 34.2% of the total amount of abrasive cloth.

The top three exporters of sandpaper are Vietnam, India, and the United States, accounting for 26.5% of the total amount of sandpaper.

The top three exporters of other substrate coated abrasives are Vietnam, Hong Kong, and the United States, accounting for 68.3% of the total.

It can be seen that the export volume of coated abrasives in China has decreased but the export value has continued to increase, indicating that product quality is steadily increasing and has certain competitive advantages and needs in the international market. Vietnam is the largest exporter of coated abrasives in China, with an annual export volume of US$409.9 million, accounting for 14.8% of total exports.

2. Imports continued to decline.

The import volume of coated abrasives was 19.4 million tons, a decrease of 6.9% year-on-year. The import amount (slightly) and the unit price of imports (slightly) increased by 2.8% year-on-year.

Imported other substrates coated abrasives accounted for the highest proportion, accounting for 50.7% of the total imports of coated abrasives, the amount (slightly), unit price of 26.53 US dollars / kg.

Imported sandpaper accounted for 26.9% of the total imports, the amount (slightly), the unit price of 8.04 US dollars / kg.

Imported sand cloth accounted for 22.4% of the total imports, the amount (slightly), the unit price of 7.52 US dollars / kg.

From the source of imported abrasives imported from China:

The top three imports of emery cloth are South Korea, Japan, and Germany, accounting for 64.4% of the total imports of emery cloth.

The top three imports of sandpaper are Japan, South Korea and the United States, accounting for 52.4% of the total imports of abrasive cloth.

The top three importers of other substrate coated abrasives are Japan, China, and the United States, accounting for 55.3% of the total.

It can be seen from the above data that the demand for high-grade other substrate materials for grinding abrasives and sandpaper is relatively large. The continuous decline in the volume of imports and imports indicates that the market share of imported products has been restricted to some extent with the improvement of the quality of domestic coated abrasives. Japan is the largest import source of coated abrasives in China, with an annual import volume of 49.73 million US dollars (the second is South Korea 45.23 million US dollars), accounting for 21.1% of the total.

3. Looking at the foreign trade situation of China's coated abrasives from the situation of the import and export volume of the abrasives industry in 2015.

China's abrasives exports in 2015 compared with the previous year (100 million US dollars)

Exports of coated abrasives and superhard abrasives have maintained steady growth. Coated abrasives accounted for 31.1% of the total exports of the three abrasives, accounting for 6.19% of the total exports of abrasives.

In 2015, China's imports of abrasives compared with the previous year (100 million US dollars):

Coated abrasives are the main varieties of abrasives imported from China. Coated abrasives account for 44.5% of the total imports of three abrasives, accounting for 39.3% of the total imports of abrasives, indicating that China's high-end coated abrasives market is at this stage. Big.

Third, the industry operation analysis

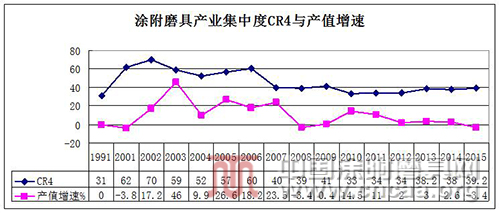

(I) Analysis of market structure 1. Industrial concentration : Industrial concentration refers to the total output value, income, output, total assets, etc. of the top 4 (CR4) or top 8 (CR8) in the industry. proportion. Because the overall size of the coated abrasive industry is small (less than 6 billion), CR4 data is used when analyzing industrial concentration. Classified according to Bain market structure:

Oligo-occupy type I CR4≥85 oligo-occupy type II 75≤CR4<85

Oligo-occupy type III 50≤CR4<75 oligo-occupancy type IV 35≤CR4<50

Oligo-occupied V-type 30≤CR4<85 Competitive CR4<30

According to the sales income, in 2015 China's coated abrasive industry CR4 was 39.2, belonging to the oligopoly v-type, the market concentration is not high (according to relevant research, China's manufacturing industry concentration is 60> CR4 ≥ 40 is better).

2. Herfinclahl-hir schman index (HHI): is expressed as the sum of the squares of the market shares of all companies in a particular market.

The US Department of Justice uses HHI as an indicator to assess the concentration of an industry and sets the following criteria:

High oligopoly type I: HHI ≥ 3000

High oligopoly type II: 3000>HHI≥1800

Low oligopoly type I: 1800>HHI≥1400

Low oligopoly type II: 1400>HHI≥1000

Competition type I: 1000>HHI≥500

Competition Type II: 500>HHI

In 2015, the data of China's coated abrasive industry HHI=517 is calculated, which belongs to the competition type I.

It can be seen from the above two indicators that the concentration of China's coated abrasives industry is not high at this stage, and there is a downward trend. This is related to the development stage of the industry. In recent years, due to the small entry barriers of the industry, the advantages of latecomers are obvious, and the “free ride†effect of post-entrants in product development, marketing, employee training, and basic investment is rapid. The expansion of the occupation of the market and the formation of a competitive situation in which thousands of sails competed for the first time led to a decline in the market share of the original oligarchic enterprises, thus affecting market concentration.

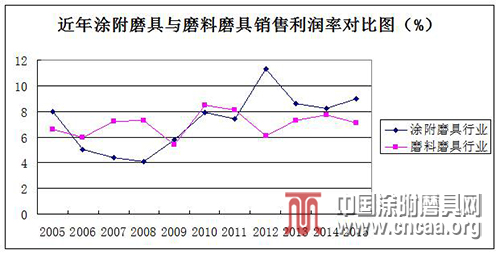

(II) Analysis of market performance and international competitiveness 1. Sales profit rate :

The sales profit rate of China's coated abrasive industry is shown in the figure below. It can be seen from the data that before 2006, it was higher than the average level of the whole abrasives industry. After the market competition increased, the profit rate decreased. After 2012, it was higher than the average level of the abrasives industry, indicating the industry's The overall manufacturing level has been improved and the profit margin has increased. In 2015, the industry sales profit rate was 9.03%.

2. Total asset contribution rate:

Total asset contribution rate (%) = (total profit + total tax + interest expense) / average total assets × 100%

Calculated by the 2015 industry year data: the industry's total asset contribution rate is 13.6% (higher than China's machinery industry standard 10.7%).

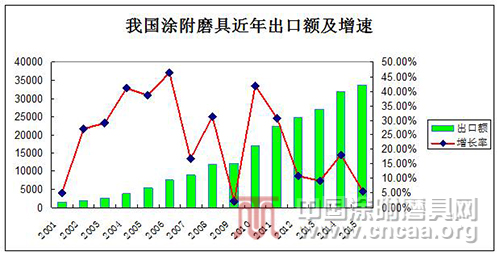

3. Product export growth rate:

In the past 15 years, the average growth rate of China's exports has reached 24.1%, exceeding the average growth rate of 16.3% of the industry's output value. In 2015, the total export value (slightly) of US dollars accounted for 41.2% of sales revenue.

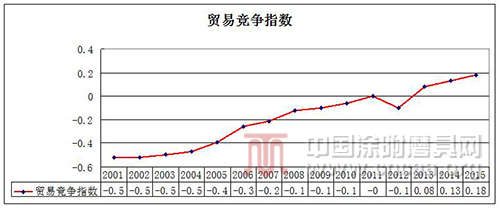

4. Trade competition index:

The trade competition index refers to the ratio of the difference between the import and export trade of products to the total volume of import and export trade. The larger the index, the stronger the international competitiveness. Indicate whether the product is a net importer or a net exporter, and the net import or export is the right size.

The trade competition index is: (Ei - Ii) / (Ei + Ii)

Ei-export volume Ii-imports In general, the index at (-1,-0.6) indicates a great competitive disadvantage, and there is a greater competitive disadvantage at (-0.6,-0.3). -0.3, 0.3) has a weak competitive advantage, has a strong competitive advantage at (0.3, 0.6), and has a strong competitive advantage at (0.6, 1).

From the data of the coated abrasive industry, it can be seen that the international competitiveness is constantly improving. The trade competition index reached a new high of 0.18 in 2015, but it is still lower than the overall 0.24 (2015) data of China's electromechanical industry. obvious.

5. Export Deterioration Advantage Index:

The export deterioration advantage index is defined as: g = (a commodity export growth rate Gi - national total export growth rate Go) X100.

The index compares the export growth rate of a particular product with the country's overall export trade growth rate, and judges whether the product has strong or weak international competitiveness during a period.

According to the value of g, it can be divided into 4 categories:

Category 1: g>10, which is a strong competitive advantage;

Class 2: 0 ≤ g ≤ 10, which is a weak competitive advantage;

Category 3: -10 ≤ g ≤ 0, which is a weak competitive disadvantage;

Category 4: g <-10, a strong competitive disadvantage.

As can be seen from the following figure, with the improvement of industrial equipment and technology level in the new century, China's coated abrasive industry has a strong competitive advantage in the international market and has shown a good development momentum.

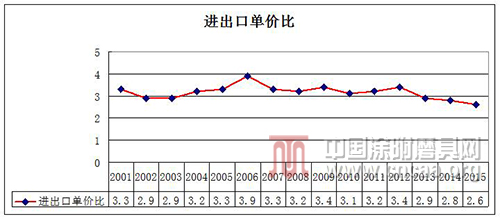

6. Import and export price ratio:

Import and export unit price ratio = import price / export price. It can indirectly reflect the quality grade (added value) of China's export products. In the past fifteen years, although the number of coated abrasive products exported in China has been greatly improved, the structure has not changed much, mainly in the middle and low-end products, and the price is the most important competitive advantage. However, the unit price ratio of import and export in the past three years has continued to decline, indicating that the gap between export products and imported products is gradually decreasing.

Fourth, the main problems

In 2015, enterprises generally felt that the decline in economic operations exceeded expectations. The lack of market demand, the decline in orders, the continuous decline in prices, and the decline in profits have become common concerns for enterprises.

First, the industry structure adjustment lacks policy support, the industry entry threshold is low, the production capacity layout is not scientific and reasonable, the elimination backwardness is insufficient; the capacity utilization rate is low, the low-end products still occupy the market leading, the homogenization competition is fierce, and the product standard level is low. Non-standard products flood the market.

Second, the industry lacks coordination and self-discipline. Enterprises are pressing each other's prices, vicious competition is intensifying, product prices continue to decline, and profitability is low. Enterprises generally survive in the vicious circle of homogeneous competition and low-price competition.

Third, the industry's ability to innovate is insufficient. Although there have been many new products in the industry in recent years, there are not many originality of autonomy. Most of them are tracking similar foreign products, and the basic and systematic research on coated abrasives is not enough. Investment in product innovation and technology has not formed the core competitiveness of products, and is still in a passive role in many fields in competition with high-grade coated abrasives in developed countries.

V. Suggestions for measures

1. Reasonably control the growth rate of production capacity and actively adjust the product structure. The Chinese economy has gradually bid farewell to the low-cost era. In the past, it has become increasingly difficult to adapt to the current development environment by simply relying on large-scale production and implementing low-cost competition to obtain profits. The industry must keep up with the pace of China's economic transformation and adjustment, rationally control the growth rate of production capacity, actively adjust the product structure, continuously improve product quality and added value, and focus on market demand, continuously improve the level of technical equipment and application research and development, and achieve health science. development of. The merger and acquisition will be the only way for the industry to control production capacity.

2. Implementing refined management, focusing on intelligent and automated development With the continuous improvement of energy, environment and labor costs, enterprises should solve the problem of energy conservation and environmental protection on the one hand, and ensure that the development of the industry will not be constrained by increasingly serious energy and environmental problems. On the other hand, it is necessary to do a good job in the cost control of raw materials, production, transportation and other aspects to ensure the profit margin of products.

To this end, enterprises must continually optimize production processes, improve equipment levels, improve product quality, do a good job in personnel training, and fully implement refined management. On this basis, the whole industry should actively implement industrial automation and intelligent development, and actively change the production, operation and sales models of enterprises to meet the arrival of the fourth industrial revolution.

3. Actively carry out applied research and continuously expand the new space for industry development.

Technological innovation has become the main driving force for social and economic development. Industry enterprises should abandon the business model of blindly following the trend and implementing homogenization competition, and actively carry out differentiated operations. Actively follow up the upgrading of traditional industrial application requirements and application innovation of emerging industries, develop market application research and new product development, meet the needs of personalized and professional applications in the downstream market, actively expand new space for enterprise and industry development, and ensure the profit level of the industry. Stable improvement.

Although the current domestic and international economic situation is still not optimistic, it should be seen that the supply-side reform, China Manufacturing 2025 and other hidden opportunities will inevitably bring transformation, upgrading and innovation-driven trends to the industry, which will also be a big wave of industry and self-innovation. Big baptism, whether it is a large enterprise or a small enterprise, as long as it focuses on innovation and continuous upgrading, it will bring a broader space for the progress of the industry and seek a bigger stage for its own development under the strategy of building and manufacturing a strong national strategy.

Aluminum Alloy Handle,Aluminum Alloy Door Handle,Hardware Wire Drawing Handle,Interior Door Handle

Guangzhou Junpai Hardware Co., Ltd , https://www.junpaihardware.com